Yulia Pavliuk is a financial content writer with a background in language, education, and clear communication. She creates SEO-friendly articles that make complex finance topics like ETFs and forex signals clear and accessible, with a strong focus on UK audiences.

Advertising Disclosure

We may receive compensation from our partners for placement of their products or services, which helps to maintain our site. We may also receive compensation if you click on certain links posted on our site. While compensation arrangements may affect the order, position or placement of product information, it doesn’t influence our assessment of those products.

Monzo helped reshape what Britons expect from a current account. With its app-based controls, instant notifications, and distinct coral card, it led the charge in digital banking. But in 2026, Monzo’s dominance is no longer assured. Recent changes in fees, tiered features, and patchy support have prompted many users to consider switching.

If you’re looking for an account that better rewards your spending, offers stronger savings rates, or simply feels more aligned with your day-to-day banking needs, you’re not short of options. A wave of challengers now matches Monzo’s tech-friendly design while offering their take on what a modern bank should be. Here’s how the most compelling Monzo alternatives stack up in 2026.

In This Guide

Starling Bank

Starling is widely seen as Monzo’s most direct competitor. Both are UK-based, app-only banks offering current accounts with instant notifications and intuitive budgeting tools. But where Monzo leans into community features and early product releases, Starling feels more mature and quietly reliable.

Standard accounts have no monthly fees, and its customer service regularly outperforms rivals. Users can set savings goals via Spaces, access overdrafts or loans on clear terms, and even manage accounts from a desktop, which is still missing from Monzo’s offering.

Fully licensed and FSCS-protected up to £85,000, Starling suits those who like Monzo’s tech-savvy edge but prefer a more stable, less experimental banking experience.

Chase UK

Chase entered the UK market with the backing of JP Morgan and a clear goal: to offer a smooth, reward-focused banking experience built entirely around the mobile app. With no branches and no plans to introduce them, Chase puts its energy into a clean interface and user-friendly features.

Cashback is one of the main draws. Users earn 1% on everyday spending within set limits, without needing to opt in or go through any additional steps. There’s also 5% interest on round-ups, allowing small purchases to build meaningful savings over time. Foreign spending is fee-free, which adds appeal for travellers or anyone shopping internationally.

Security is another strength. Virtual card controls are easy to manage, and in-app features have been designed with privacy in mind. While the account currently lacks joint access and overdraft support, Chase continues to add functionality at a steady pace.

For those seeking a straightforward alternative to Monzo with genuine perks and minimal friction, Chase stands out as a credible, high-reward option.

Revolut

Revolut began life as a low-cost alternative for exchanging foreign currencies, but it has since evolved into a broad financial platform. Today, it offers current accounts, investment products, cryptocurrency access, and travel benefits, depending on your subscription tier.

Its main appeal lies in flexibility. Users can hold and spend in over 30 currencies, track spending with built-in analytics, and even trade stocks and commodities, all within a single app. These features make Revolut especially popular among digital nomads, frequent travellers, and those curious about dabbling in modern finance without opening multiple accounts.

Many of Revolut’s more advanced features (such as priority support, higher ATM limits or travel insurance) are only available on paid plans. For those who mostly bank in pounds, the value proposition can vary.

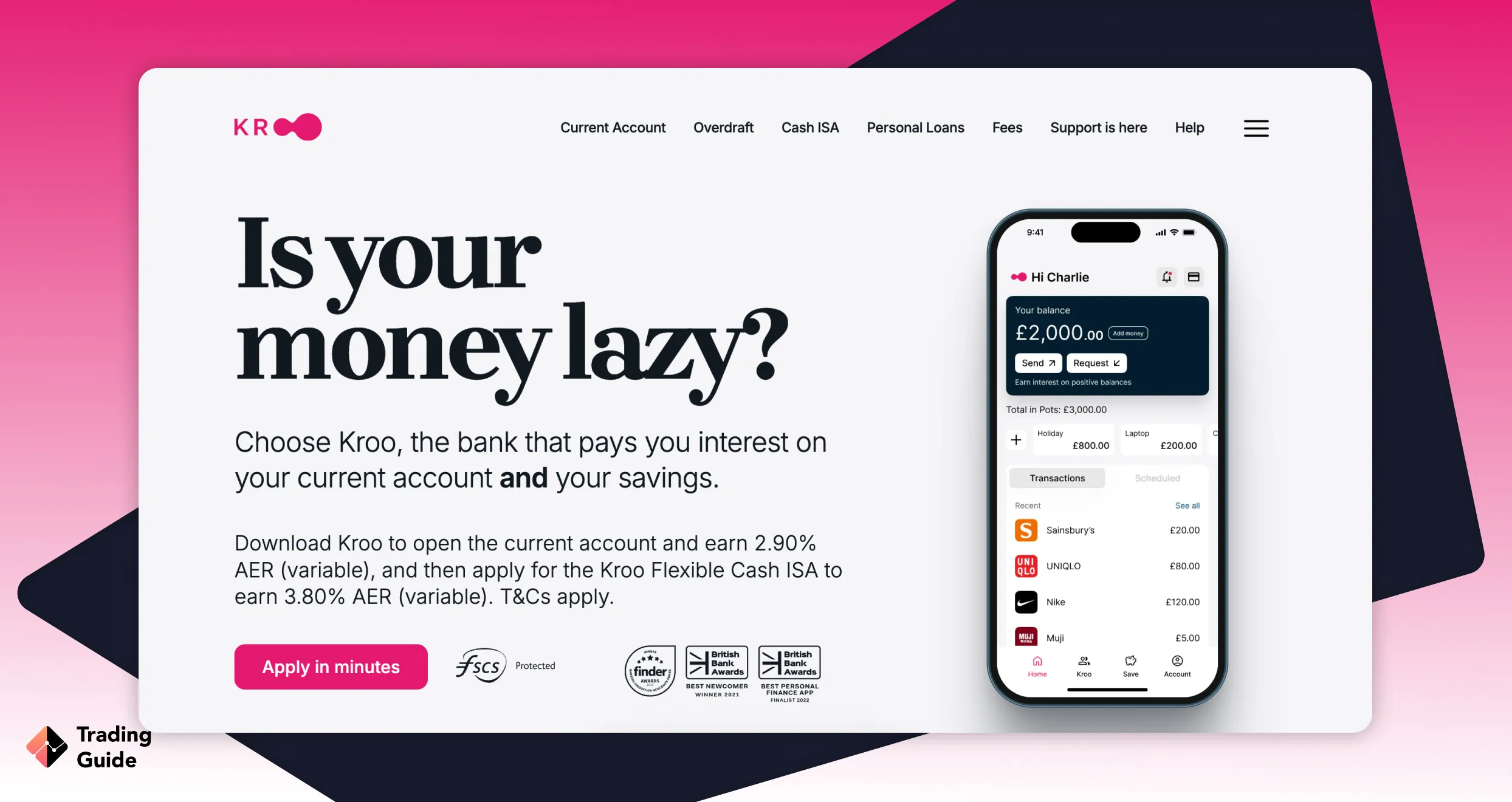

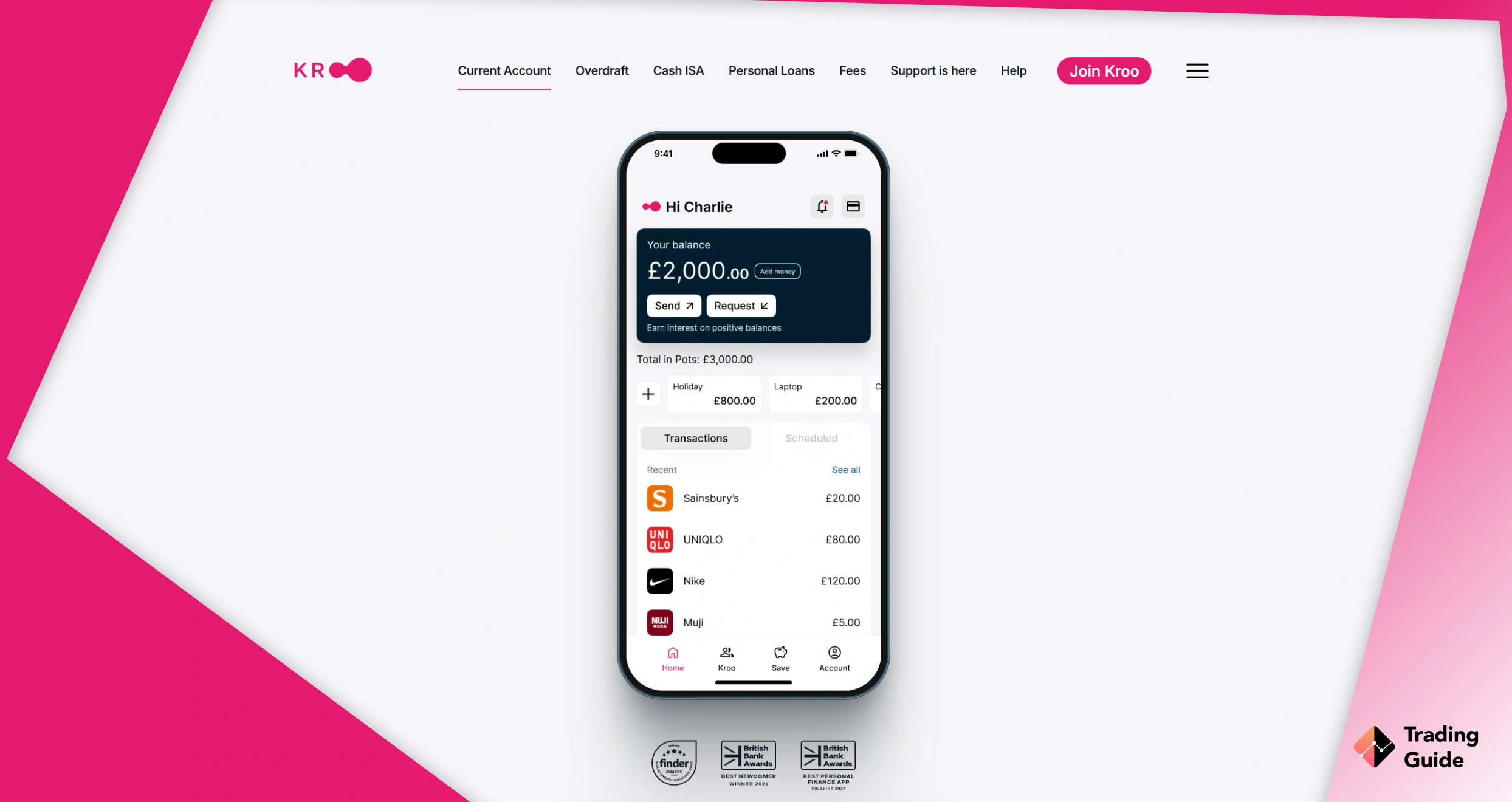

Kroo

Kroo positions itself as the eco-conscious alternative to legacy banks, offering a digital-only current account with an environmental edge. Users earn interest on their balances at rates that rival traditional savings accounts, and the app includes carbon-tracking tools designed to nudge greener spending habits.

Group features are well thought out. Shared tabs and bill-splitting tools feel seamless, while the overall interface is modern and responsive. While Kroo is still expanding its feature set, it already feels like a strong fit for those who want their banking to reflect their values, without giving up usability or speed.

Kroo appeals to users seeking ethical banking without compromising on function.

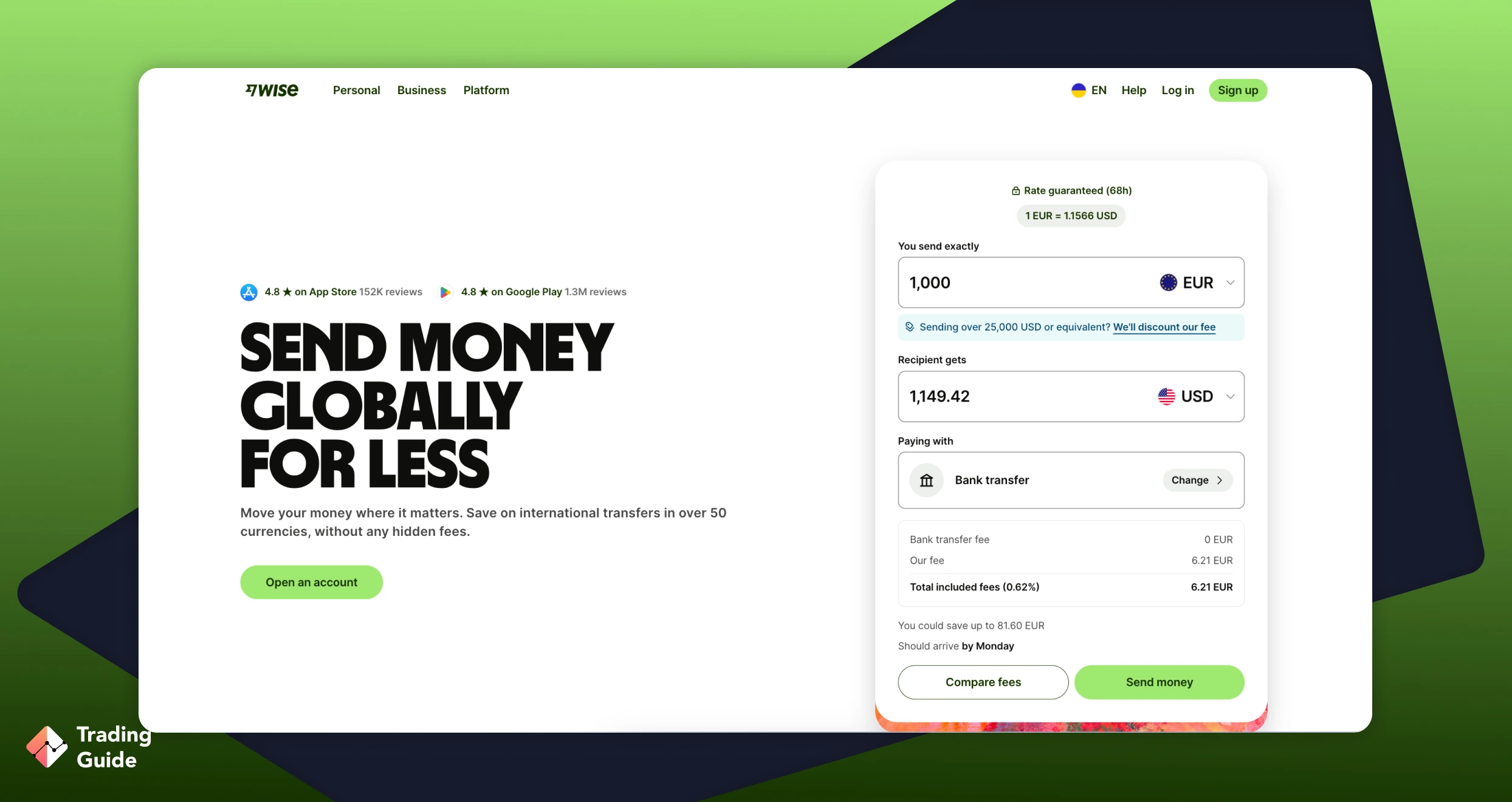

Wise

Wise, formerly known as TransferWise, isn’t a bank in the strictest sense, but for those who deal in multiple currencies, it often outperforms one. Its core strength is cross-border functionality: users can hold, send, and spend money globally with minimal fees and real exchange rates.

The platform offers UK account details, a debit card for everyday use, and tools designed for freelancers or businesses that work with international clients. For travel, Wise offers one of the most cost-efficient ways to pay abroad, with transparent fees and strong currency conversion.

It lacks traditional credit products like overdrafts or loans, and there’s no FSCS protection. However, for those who regularly operate across borders, Wise delivers precision and control that most high-street banks still can’t match.

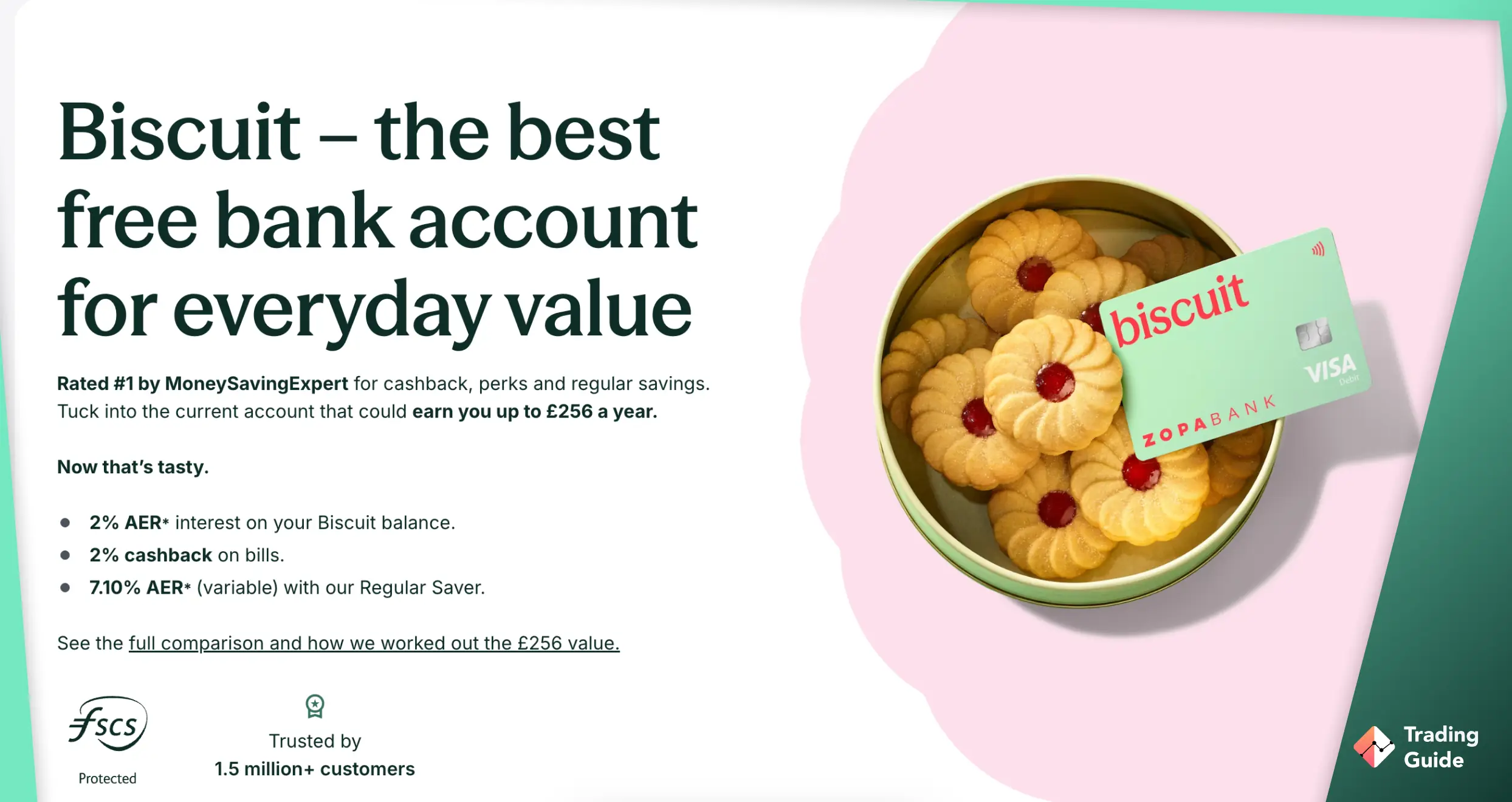

Zopa

Zopa has transitioned from a pioneer in peer-to-peer lending to a fully regulated digital bank, focusing on savings and borrowing. Although it doesn’t offer a standard current account, it earns its place as a complementary option, particularly for users seeking better interest on savings or fairer access to credit.

Its fixed-rate savings products regularly top best-buy tables, and the Smart Saver feature lets users earn interest while retaining instant access. Zopa’s personal loans and credit cards are equally competitive, often with lower APRs than mainstream rivals.

With no account fees and a clean, app-based interface, Zopa functions best as an add-on rather than a standalone bank, ideal for building a savings habit or consolidating borrowing without disruption to your main current account.

Comparing Features

Choosing an alternative to Monzo means looking beyond branding and focusing on the features that genuinely affect your day-to-day banking. Below is a snapshot of how the main contenders compare on core criteria:

The right choice comes down to what you value most: interest, rewards, simplicity, ethics, or flexibility. There’s no single winner, only the best match for your money habits.

| Provider | Monthly Fee | FSCS Protection | Interest on Savings | Budgeting Tools | Rewards |

|---|---|---|---|---|---|

| Starling | None | Yes | Yes (via Spaces) | Yes | None |

| Chase UK | None | Yes | 5% (round-ups) | Limited | 1% cashback |

| Revolut | Free–£12.99 | Partial (paid plans) | Yes (varies by tier) | Advanced | Premium only |

| Kroo | None | Yes | 4.35% AER | Yes | None |

| Wise | None | No (but regulated) | No | Basic | None |

| Zopa | None | Yes | Yes (fixed and flexible) | No | None |

Rethinking Monzo

Monzo still draws loyalty for its intuitive budgeting tools and features like Pots. But limitations around joint accounts, support delays, or lacklustre international functions are pushing some users to explore more responsive or rewarding alternatives.

Fortunately, switching banks is easier than ever thanks to the Current Account Switch Service. It’s often wise to test a new account alongside Monzo before committing fully, especially if you rely on direct debits or salary payments. Many users now adopt a blended approach, using Monzo for everyday spending and pairing it with Starling, Chase, or another provider for cashback, savings, or travel benefits.

Whether you stay or move on, the key is choosing a bank that keeps pace with your financial habits, not one that makes you feel stuck.

FAQs

Can I have more than one digital bank account in the UK?

Yes, you can open multiple digital accounts as long as you meet each provider’s eligibility. Many users pair apps to split spending, savings, and subscriptions.

Are these Monzo alternatives safe to use?

Most are UK-regulated and covered by the Financial Services Compensation Scheme (FSCS), which protects deposits of up to £85,000.

Do Monzo alternatives charge for overseas spending?

Not always. Chase and Wise are strong on overseas charges, while Revolut’s free tier includes some foreign use. Always check the latest limits and fees before you travel.

Which Monzo alternative is best for saving money?

If high interest is your goal, Kroo and Chase currently offer strong rates. For more structured savings tools, Starling or Zopa might be a better fit.

Final Thoughts

Monzo helped set the standard, but the market has matured. Today’s best alternatives don’t just match its features; they improve on them in ways that may better suit your financial habits. Whether it’s cashback, savings rates, or global use, switching no longer means compromise.

The strongest options now offer clear value for specific needs, from ethical banking to international payments. As digital finance becomes more specialised, choosing the right account is less about brand and more about fit.